Russia-Ukraine war raises stagflation risks

Remain overweight commodities. Add gold to hedge against stagflation tail risk, funded by increased underweight in equities

Russia-Ukraine war will lead to higher inflation, complicating an already difficult year for central banks: While Russia and Ukraine are not large economies by themselves, they are significant producers of a whole host of commodities, ranging from oil, gas, wheat, corn, sunflower oil, nickel, palladium, aluminum, and many more. The combination of the devastation in Ukraine, sanctions on Russia and uncertainty around their implementation, coupled with supply-chain disruptions have pushed up commodity prices to highs last seen in the early 2010s. If sustained, this will raise costs for consumers and companies around the world, while adding further to inflation problems already plaguing global central banks’ interest rate policy.

Commodity prices are likely to remain high even if the war ends quickly: We think the supply-side impacts from the war are not easily resolved. As such, they can last for some time even in a best case scenario. First, sanctions against Russia (and the threat of them) are unlikely to be removed or ramped down soon by the West, short of a drastic change within Russia. As such, buyers and financiers of Russian commodities will continue to be wary and “self-sanction” to some extent. Second, it will take time to restore production disruptions in Ukraine, including in the important agriculture sector. Third, many of the recent divestment decisions by oil companies from Russia are not easily reversible and are likely permanent. The broader context is that inventories of many commodities were already very tight, and the latest developments add further fuel to the inflation fire.

Chart 1: A whole host of commodity prices including crude oil and wheat surged to new highs

The balance of risks to growth are now tilted towards the downside, especially in Europe which is closer to the source of conflict. Our base case is for global growth to slow more than we initially expected due to the Russia-Ukraine war, but remain at a decent clip. While higher prices will crimp spending and impact corporate margins, it is important to note that household and corporate balance sheets are still robust due to sizeable fiscal and monetary stimulus, while labour markets in key developed markets are strong (perhaps somewhat too strong). In addition, many economies are reopening as COVID becomes more endemic. Nonetheless, it remains extremely difficult to predict how the war might pan out through the year and as such prudence is required. Key risk scenarios to the growth outlook include further sharp increases to oil prices perhaps above US$130/bbl, a meaningful disruption to gas supplies in Europe unilaterally by Russia, and/or a broad-based tightening in financial conditions such as through a much stronger US Dollar.

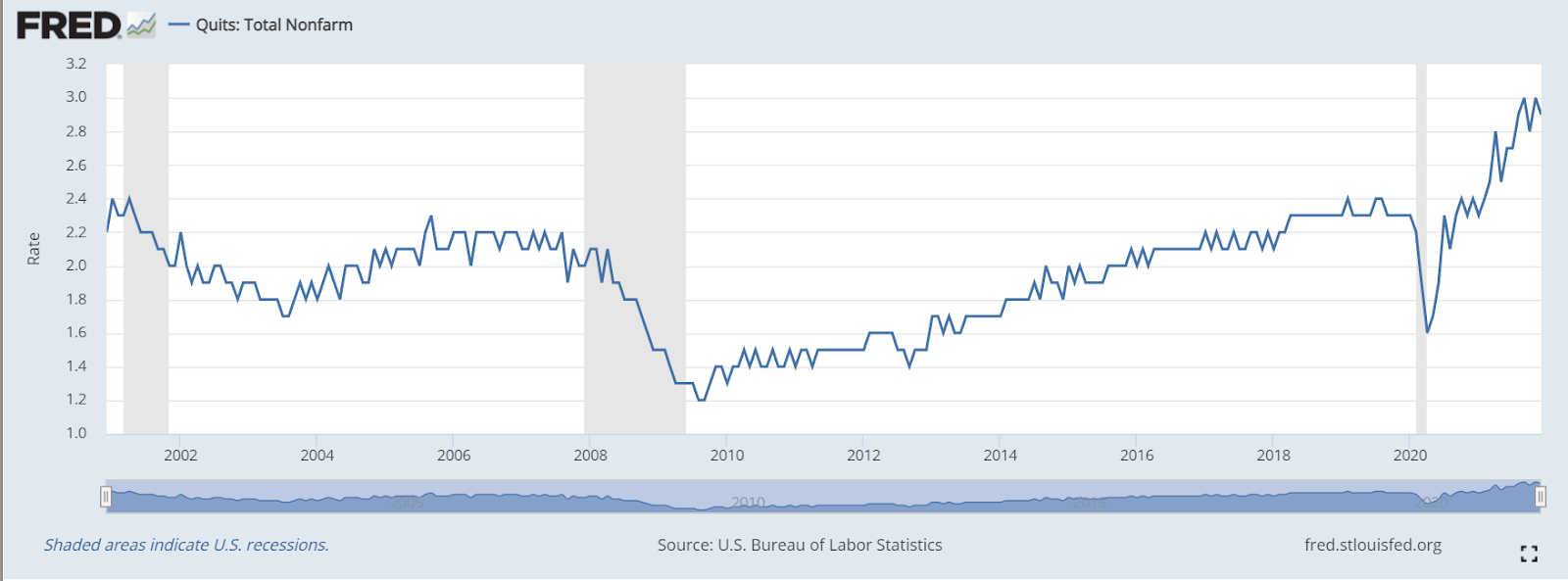

Supply-driven commodity shock raises the spectre of 1970s style wage-price spiral given historically tight US labour markets. Crucially, the commodity supply shock is coming at a bad time. The US is already overheating to some extent with a historically tight labour market, broadening inflation pressures, and still extremely accommodative fiscal and monetary policy. Further rise in price pressures could start to unanchor inflation expectations, leading workers to require higher wages to remain in the labour market. The longer the Fed waits to tighten policy, the greater the risk of such a wage-price spiral. While the 1970s stagflation episode comes to mind, key differences which make us somewhat less worried include the weaker role of labour unions and a stronger US Dollar. Overall, we expect the Fed to hike rates steadily through 2022 and announce balance sheet reduction by July, with the risk tilted towards a faster pace of tightening into 2023 barring a recession.

Chart 2: The US labour market is extremely tight with quit rates and job openings at record highs, raising concerns about an overheating economy

Chart 3: The 1970s period was characterised by high inflation rates and rising unemployment

US Dollar to strengthen further in 2022; CNY could remain a relative safe haven: We have been expecting the US Dollar to strengthen in 2022 as the Fed turns more hawkish, but partially offset by policy tightening from non-US central banks. Nonetheless, the Russia-Ukraine war raises concerns surrounding global growth in the near-term and as such, is a further supportive factor to my strong Dollar view this year. Among major currencies, the CNY could continue to be a relative safe haven given China’s strong current account surplus, rollout of stimulus, coupled with increasing inflows into its sovereign bond markets as investors seek for alternatives.

Will King Dollar eventually lose its luster? Longer-run macro impact from Russia-Ukraine war worth contemplating: While it’s still too early to predict how exactly the war will turn out, there are already signs of seismic shifts which could have an impact on the global economy for many years to come. These include:

Concerns around the US Dollar’s excessive dominance could rise further. The sanctions imposed by the West have effectively made the Russian central bank’s US Dollar foreign exchange reserves inaccessible and worthless through unilateral actions. Central banks around the world, especially China’s, could view this development with substantial concern and seek to diversify their reserves further away from the US Dollar.

Crypto adoption (and the regulatory response) could be accelerated further. The sanctions and domestic capital controls have resulted in a surge in usage of crypto, both as a way to circumvent sanctions and controls while maintaining a store of value, and also as a way to easily raise funds and donations (see link). Regulators are also taking notice, especially with respect to sanctioned individuals (see link). Whether this ultimately results in crypto becoming more mainstream and perceived as a "responsible" player remains to be seen.

The interaction between climate change and energy security will continue to become more salient, especially for Europe. In the near-term, this will likely lead to investments in LNG terminals and perhaps also restarting of nuclear power plants to diversify away from Russian gas. Over the medium term, countries could further accelerate plans to move towards renewable energy (see link).

Deglobalisation accelerated: While the Russia-Ukraine war has indirectly brought NATO closer together, it has also brought about significant divisions both within and across countries. The longer-term impact could be to accelerate the deglobalisation trend in place post-GFC, in both the physical and digital realms.

My key investment recommendations include:

Remain overweight in commodities, a position I have held since early 4Q.

Add gold position to hedge against stagflation tail risks

Fund gold position by increasing underweight in equities (in particular Europe and US equities)

Remain underweight credit

Remain strong underweight government bonds

Remain overweight cash