Will there be a sustained inflation rise, and will the Fed respond in kind?

Inflation pressures likely to be transient, reflecting short-term supply-side constraints rather than overheating of the economy

In recent weeks, concerns over a sustained inflation rise and as a consequence, faster than expected Fed tightening, have risen in the markets.

This is in part due to the significant size of the Biden administration's latest stimulus package (US$1.9 trillion or 9% of GDP) relative to official estimates of the output gap (around 4% of GDP by the CBO's estimates), and coming at a time when households have already accumulated significant excess savings from past fiscal packages (see here and here for instance).

Meanwhile, a whole host of price indicators, ranging from hard and soft commodity prices to container freight rates have surged over the last six months, leading many to believe that we might already be entering a new inflation regime. The 10 year US Treasury yield has risen above 1.5%, while the US dollar has also strengthened over the past two weeks.

My judgement at this point in time is that inflation in the US will rise somewhat this year, partly reflecting base effects, capacity constraints in the goods sector, and some teething issues as the US economy reopens post vaccinations.

However, this rise will likely be transient, reflecting short-term supply-side constraints rather than overheating of the economy. As a result, I believe the Fed will be able to look past it and stay accommodative for longer.

There are three key reasons underpinning my view.

First, the US economy probably has more spare capacity than what the headline output gap measures are suggesting.

Potential GDP is a notoriously difficult measure to ascertain. As one evidence, the Congressional Budget Office has consistently downgraded its estimates of potential GDP for 14 straight years from 2007 to 2021 (see link here).

I think elevated unemployment rates are a better reflection of the level of slack in the US economy. Even here, the “true” level of the unemployment rate could be closer to 10% instead of 6%, if we take into account those who dropped out of the labour force temporarily due to the pandemic (see Chair Powell and Treasury Secretary Yellen’s references here and here on this point).

Second, capacity constraints in the goods sector should ease up as service sectors reopen.

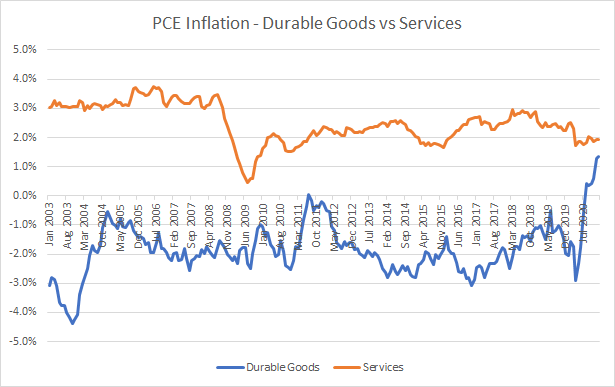

There is a huge divergence right now between goods and services demand globally. This is especially pronounced in the US (see chart below).

Part of this is due to continued mobility restrictions, leading to excess demand in the goods sector. As an extremely simplistic example, people are diverting some of their spending to massage chairs and consumer electronics instead of going to restaurants and bars due to lockdowns (see Guerrieri et al (2020) for a theoretical illustration of this concept). Nonetheless, a good chunk of the goods demand increase is probably more durable and structural due to tech investments.

My expectation is that as vaccination progresses in developed markets, incremental pent up demand will increasingly shift away from goods and towards services. This should lead to some relief in price pressures in areas such as container freight rates and commodity prices as we move into 2H of the year.

Third, labour supply seems to be flexible enough to fill pent-up demand in the services sector, based on early indications.

The latest payroll numbers in February shows a sharp rebound in the sectors most negatively impacted by the virus such as leisure and hospitality as the economy started to reopen. Crucially, this bounce came with little signs of a sharp bid in wages, at least so far (see link here).

As the US economy reopens over the rest of this year, how easy it is to supply service sector jobs will be crucial to the evolution of services inflation. My expectation is that this should be fairly easy given the significant slack in the labour market (as mentioned above).

One of the largest sources of uncertainty to my benign view is how quickly US consumers will spend out of their excess savings (see here and here). Latest estimates show that US consumers probably spent between 25-40% of the cash transfers from earlier stimulus rounds.

If consumers start to spend down their savings and transfers at a higher clip and faster rate, this could stoke demand pressures relative to what the economy could supply in the near-term, leading to stronger price pressures.

Source: Getting back to a strong labour market (Chair Jerome Powell - see link)