Hawkish Fed, modestly stronger US Dollar in 2H21

Reduce overweight to stocks, increasing some allocation to cash, removing hedges for weak US Dollar

The Fed turned hawkish in the June meeting, and is now less tolerant of higher inflation than we had expected: The latest FOMC meeting was one of the most consequential ones for asset markets and the US Dollar outlook since the COVID-19 crisis began. While the Fed's forecasts continued to imply (on paper) that it views this year's inflation rise as temporary, its dot-plot projections suggest it is not willing to tolerate rising inflation as much as ourselves and the market had expected. Note that the Fed's newly implemented Flexible and Average Inflation Targeting (FAIT) framework (see here) should have implied a much more patient Fed - one that is willing to run the economy hot for a while, is able to stomach the recent rise in price pressures, and who responds to actual rather than forecasted progress in the labour market and inflation. With that, a significant number of Fed officials pulled forward their rate hike expectations to 2023 relative to the March meeting, despite making only marginal changes to their longer-term inflation and growth projections.

Chart 1: More US FOMC participants now see an earlier and steeper path to rate hikes by 2023, despite only making small adjustments in longer-term inflation projections.

Hawkish Fed provides more support for the US Dollar. We have been calling for the US dollar to weaken moderately over 2021 on balance (see here), amidst the continued tug of war between strong US growth resulting in faster Fed rate hikes (which is US Dollar positive), and robust global growth (which is US Dollar negative) (see infographic below for three main drivers of the US Dollar). With the Fed now turning more hawkish and being less willing to tolerate price increases, one factor driving our forecast for US Dollar weakness is fading, tilting the balance marginally towards a stronger Dollar at least for now.

Strong US economic data over the next few months lends some support to Dollar strength in 2H2021: With this change in how the market perceives the Fed’s tolerance of inflation pressures post FOMC, the market could bring forward Fed rate hike expectations further if US economic data improves. This could in turn push the US Dollar stronger and also weigh on risk assets at least over the next few months into October/November. On this note, we expect the US labour market to show further improvement in the 3rd quarter, with payroll additions of around 600k-1million per month as labour supply constraints ease. We will likely see a few more firm inflation prints before prices start to normalise, and as such, year-on-year inflation rates in the US should only moderate moving into 2022.

Nonetheless, improving global growth outside the US provides an important offset to a more hawkish Fed. This informs our new base case view for only a modest rise in the US Dollar this year, and makes us still quite positive on risk assets such as equities on balance: We continue to think that global growth will remain strong this year (see here and here), which is typically associated with a weaker US Dollar. Vaccination rates continue to rise in Europe and China, and are now rising in parts of Emerging Markets from low levels (see Chart 2 below). This comes as vaccinations in the US have plateaued at around 52% of its population. As such, the bulk of the reopening boom is yet to come in countries outside the US, while the largest growth boost is probably already over in the US.

Chart 2: The bulk of the reopening boom is yet to come in countries outside the US, while the largest growth boost is probably over in the US

* Number of doses administered as a share of population, may not be equal to the total number of people vaccinated

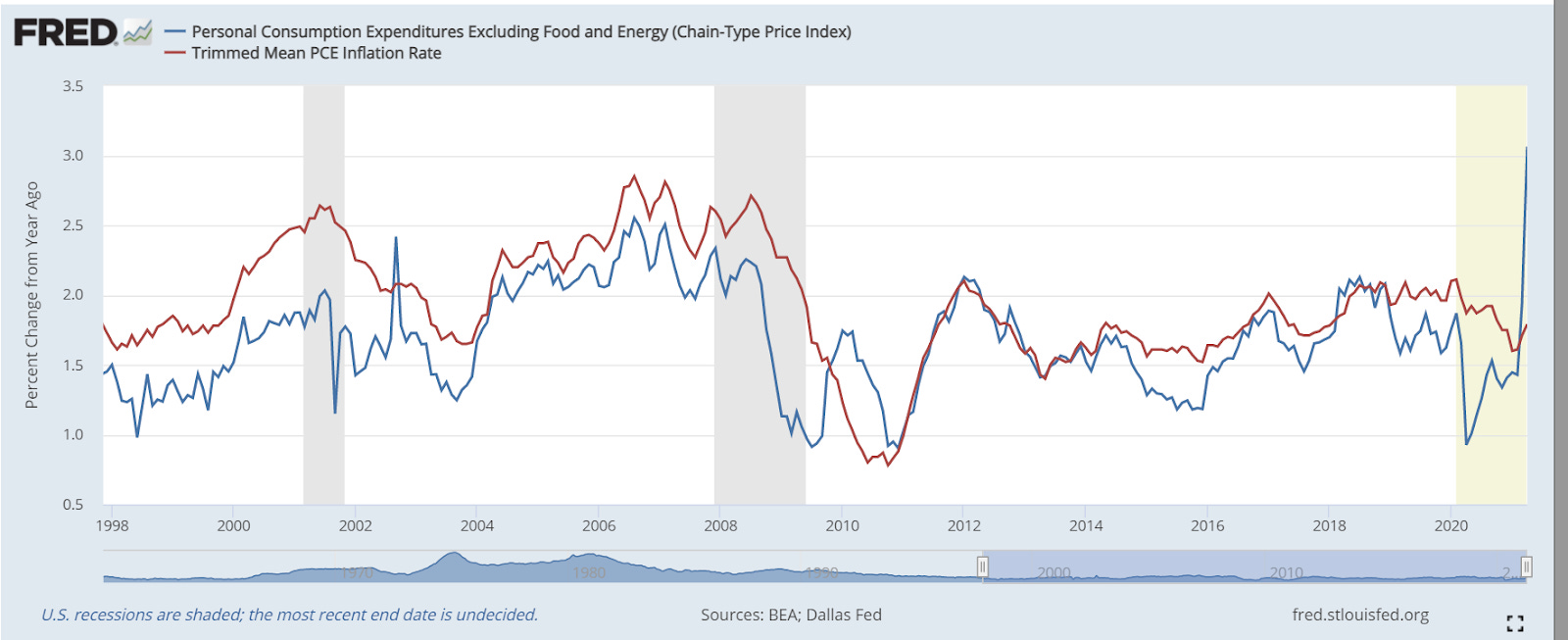

Inflation is the biggest wildcard - The US Dollar could strengthen much more if price pressures prove more persistent than we expect: We continue to view the bulk of the inflation rise this year as temporary, reflecting supply-side shortages amidst the extraordinary challenges brought by Covid-19 (see our take here). As one evidence, recent price spikes were in large part attributable to outliers such as used car prices, sporting equipment, and reopening effects, with alternative measures of inflation still showing contained underlying price pressures so far (see Chart 3 below). Significant slack and spare capacity still remains in the US labour market, with nearly 8 million unemployed relative to pre-pandemic trends. Although labour supply has been less elastic in recent months, this should improve as unemployment benefits start to expire. Nonetheless, a more persistent inflation rise than we expect could accelerate the timing of Fed rate hikes, resulting in more substantial US Dollar strength and weigh on risk assets as we move into 2022. This scenario of accelerating inflation pressures is not our base case, but is an important risk to watch out for.

Chart 3: Alternative measures of inflation which strip out outliers still show contained underlying price pressures

Source: Fred St Louis (https://fred.stlouisfed.org/series/PCETRIM1M158SFRBDAL#0)

Investment Implications

While we continue to be positive on global economic growth and risk assets, the change in the Fed’s tone and reaction function could start to weigh on returns as we move into the rest of this year.

Our base case is that inflation is transitory and the Fed will ultimately be able to look through the rise in prices. Nonetheless, risk assets could come under pressure if our view is wrong.

At the same time, prices of traditional inflation hedges such as commodities are already quite elevated. While this is not to say they won’t rise further, the value from increasing allocation to commodities could be limited at the margin.

As such, it’s probably worth having a bit more cash than usual going into the second half of the year.

The macro backdrop for 2H2021 lends me to the following implications:

Reduce overweight in Equities

Within Equities:

Reduce overweight to the US

Move Japan from underweight to neutral

Maintain underweight in China

Maintain overweight in Europe and Emerging Markets (ex China)

Increase allocation to Cash

Neutral Credit

Underweight DM Government Bonds

Less negative on duration risk

Remove hedges for US dollar weakness