Slowing China Meets Supply Constraints

Slower global growth, more persistent inflation, stronger US Dollar

I am now less positive on the outlook for the global economy moving into 2022. China’s economy is likely to slow more than expected, given the weaker property market and recent power cuts across the country. In addition, significant risks are building up for an energy growth shock in Europe given extremely tight gas inventories and soaring gas prices, which could in turn spillover to global energy prices.

In addition, inflation pressures will likely be more persistent than previously anticipated. These price pressures partly reflect unusually high goods demand running up against supply-side constraints such as semiconductor and commodity shortages, coupled with manufacturing and port disruptions. Decarbonisation initiatives are also intensifying at a time when renewable energy output has been lower than expected. Nonetheless, some (but not all) of these supply bottlenecks are likely temporary and should resolve themselves over time.

Maintain my view for the US Dollar to strengthen further. However, I now see a possibility of a more pronounced rise, given more moderate global growth, coupled with a Fed which is moving towards reducing monetary policy accommodation (see Hawkish Fed, Modestly Strong US Dollar).

I highlight several macro headwinds which have intensified in September.

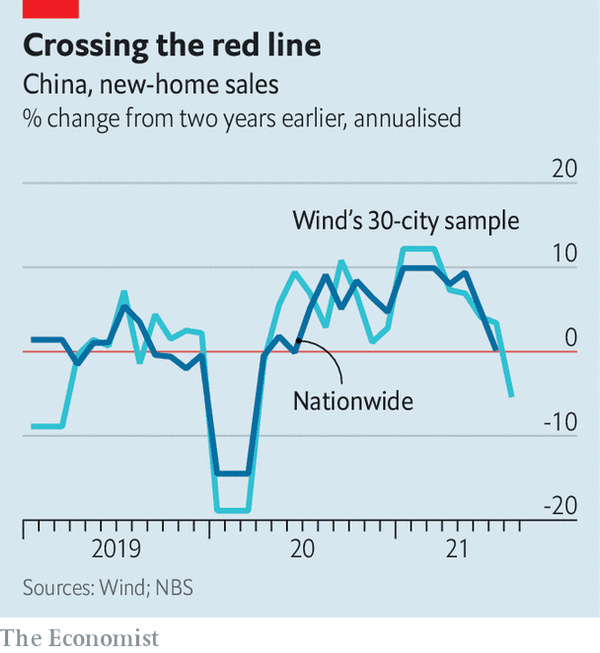

First, China's economy will likely slow down more than we had initially expected. For one, the country’s property market faces more downward pressure moving into 2022 given recent developments, and even with a base case assumption of an orderly debt restructuring of Evergrande (see Chart 1 below). In addition, many provinces in China have implemented power cuts in September, resulting in production disruptions especially in high-energy intensive sectors (see link). These power reductions in turn reflect China’s decarbonisation drive, which have intensified pressure on local governments to meet environmental targets, while also reducing power supply from coal-fired plants. The extent of China’s growth slowdown over 2022 will depend on how quickly policymakers can stabilise these headwinds to activity, while also supporting the economy through easier fiscal and monetary policy (which we expect). Overall, I think the risks to China’s growth are tilted towards the downside.

Chart 1: China’s property market has started to slow down, while power cuts have affected many provinces and energy-intensive industrial sectors across China

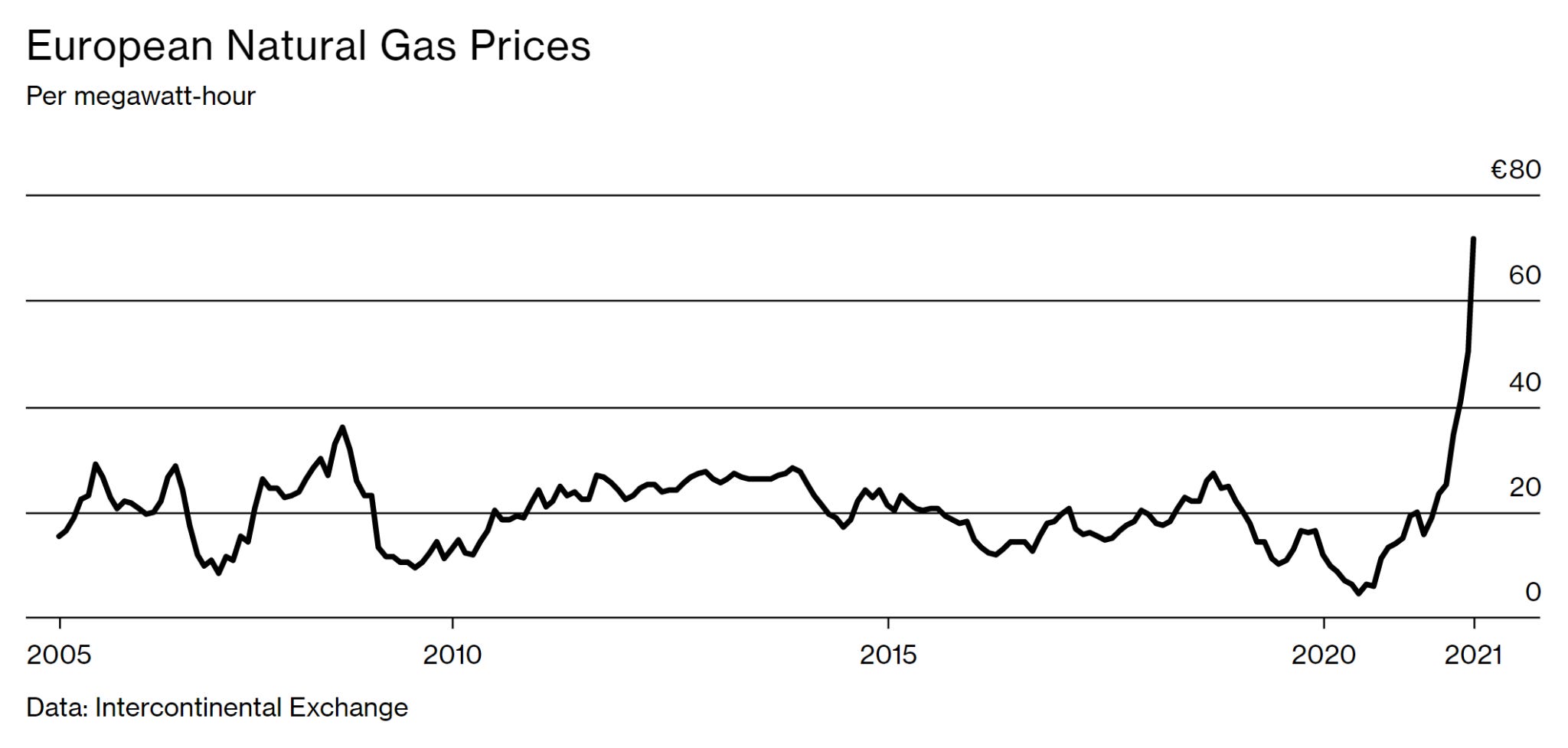

Second, the recent surge in European natural gas prices poses downside risks to European growth, and consequently, some upside risks to global energy prices. While the direct economic impact of the gas price surge is not large by itself (~20bps decline to GDP and 20bps rise in inflation), this development comes even before peak winter demand (see Chart 2 below). A colder than usual winter could cause electricity prices to rise further and even result in shortages, hitting European growth. There will likely be knock-on impact to other energy-related commodities such as oil and coal as well, which will raise input costs globally. A confluence of factors have led us to this precarious situation, including strong LNG demand from China and Brazil, disappointing offshore wind power generation in Europe, and a depletion of gas inventories due to the colder than usual winter earlier this year (see here for instance).

Chart 2: European gas prices surged more than 400%, even before the peak winter season

Third, smaller fiscal stimulus from the US looks increasingly likely, providing less support to US growth in 2022. In the very near-term, the US is trying to prevent a government shutdown and raise the debt ceiling limit (once again), which is expected to be binding by 18 October. The broader picture is that gridlock between various factions in Congress will likely hamstrung the passage of more ambitious aspects of President Biden’s fiscal support package. If we are right, this should imply a larger fiscal drag for the US economy in 2022.

Fourth, supply chain disruptions have intensified and lasted for longer than expected heading into the holiday season. Over the past few months, container shipping rates have risen further, reflecting supply-side disruptions such as Typhoon Chanthu in China. COVID waves have also continued to affect manufacturing activities out of Asian countries such as Vietnam and Malaysia, disrupting the supply chain for companies such as Nike, Adidas and Toyota (see link). Recent power cuts in China as mentioned above could also result in significant disruptions to the global manufacturing sector, especially if it broadens beyond just energy-intensive industrial sectors. All these factors could have negative spillover effects globally, including on prices and corporate margins as we move into 2022. Our base case is for some of these supply-side disruptions to resolve themselves over time, but the exact timing is uncertain.

Chart 3: Supply-side disruptions have intensified further over the past few months

Investment implications - Underweight equities, overweight cash and commodities, stronger US Dollar

Stronger US dollar, driven by slower global growth and a more hawkish Fed: We have been expecting the US Dollar to strengthen in 2H2021, but only modestly, with robust global growth outside the US helping to offset a more hawkish Fed (see Hawkish Fed, Modestly Stronger US Dollar). Moving forward, our expectation for global growth to moderate should provide even greater support to the US dollar over the next six months. In addition, the Fed could also turn somewhat more hawkish, given our expectation for US inflation to be more persistent than most analysts and policymakers expect with recent supply-side disruptions.

The overall macro backdrop moving into 2022 lends me to the following investment implications:

Turn underweight in Equities from overweight previously

Within Equities:

Maintain underweight China

Turn underweight Asia ex-Japan, especially cyclically-oriented markets. Domestic oriented markets such as Indonesia could be more resilient

Turn underweight Emerging Markets (ex China)

Turn neutral in Europe from overweight

Maintain neutral in Japan

Turn overweight commodities, especially energy-linked ones

Raise allocation to cash further

Remain Neutral Credit

Overweight global high yield, underweight Asian high yield

Underweight investment grade

Remain Underweight DM Government Bonds